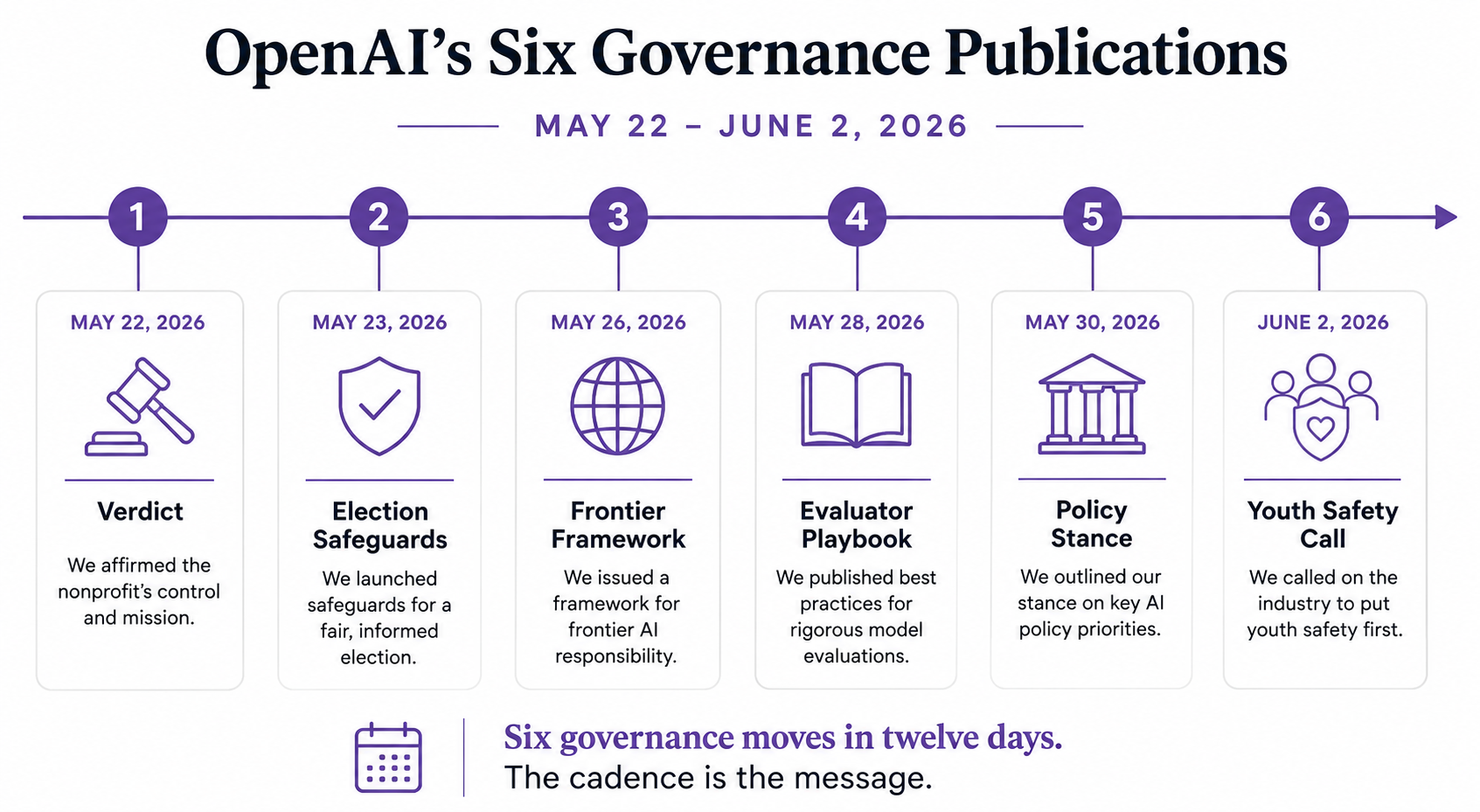

OpenAI cleared the Musk verdict on May 22 and then published five governance papers between May 27 and June 2. Six documents in twelve days, four of them aimed squarely at regulators. That’s not a content calendar. That’s the front matter of an IPO prospectus, written in public.

I’ve been watching how the frontier AI labs position with regulators, because clients in government and enterprise keep asking me which of these moves are substantive and which are signaling. The honest answer for this particular sprint is that the timing is the substance — the cadence tells you what the documents are for before you read a single one of them.

If you don’t live in the IPO-prep world every day, here’s the term that does the most work: an S-1 is the registration filing a U.S. company submits to the SEC before listing shares publicly. It’s the document where the company has to explain — to regulators and to future public investors — that the business is legal, its governance is sane, and its risks are disclosed. For a company like OpenAI, with a charity-to-for-profit conversion in its past and an EU AI Act sitting in its future, the governance section of that filing is where the IPO actually gets won or lost. Everything else is appendix.

The week that started with a verdict

A New York jury ruled for Altman in the Musk lawsuit in roughly two hours, on statute-of-limitations grounds. Musk’s core claim — that Altman “stole a charity” by converting OpenAI to for-profit — never got litigated on the merits. The verdict cleared the legal exposure, but the New Yorker’s read is the one that matters here: the trial demonstrated that governance-by-founder-character is inadequate at AI lab scale. The lawsuit went away. The structural question it raised did not.

That distinction is what makes the next five days interesting. If you read the verdict as the end of the story, the publishing cadence afterward looks like routine corporate communications. If you read it as a procedural clearing — the legal anchor lifted, but the substantive question still floating — the next five governance papers stop looking routine and start looking like an answer.

What’s inside the five papers

Five publications in seven days, in this order:

- Election safeguards (May 27). Voter information access, cyber-defense support for elections infrastructure, and AI-transparency commitments — timed for the 2026 global election cycle. Reads as “we are not the next Cambridge Analytica.”

- The Frontier Governance Framework (May 28). Maps OpenAI’s internal safety and risk practices directly to the EU AI Act and California AI regulation requirements. The mapping itself is the artifact — it’s a document examiners can read clause-by-clause against the statute.

- Third-party evaluator playbook (May 29). Standardizes how outside auditors should assess frontier models — capability assessment, safeguards criteria, validity standards. Reads as “here is how to grade us, and here is the rubric you should use.”

- AI policy and political advocacy stance (June 1). Formalizes the company’s position on lobbying, transparency, and — pointedly — that no outside political group speaks for OpenAI. Reads as “we are not a17z, and we will say so in writing.”

- Global AI Safety Institute proposal (June 2). A call for international institutional architecture focused on youth protection. Reads as “we will help build the regulator that regulates us.”

Six governance moves in twelve days. The cadence is the message.

The cadence is the message

Any one of these documents, on its own, is unremarkable. Frontier labs publish governance papers all the time. What’s distinctive here is the sequence: a legal threat resolved, then a regulator-facing document every day or two for a week, then an international-institution proposal to close the run.

The argument I’d make is that the substance of each individual document matters less right now than the cadence does. Each paper is a brick. The wall is the IPO prospectus’s governance section, and the wall is being laid in public, in a way that lets regulators and future investors watch it go up. By the time an S-1 hits the SEC, OpenAI’s lawyers will not need to argue that the company has a governance posture aligned with the EU AI Act and California regulation — they’ll be able to point to a dated PDF.

That’s a different kind of work than analysis or advocacy. It’s the work of building an evidentiary record, and the schedule is part of the record. A regulator who reads these documents in twelve months will not see “OpenAI’s governance philosophy” — they’ll see “OpenAI’s documented, dated, sequential governance commitments.” That’s a much harder thing to argue with.

What to watch next

Two things will tell you whether this read is right.

- Verbatim adoption by regulators. Watch which sentences from the Frontier Governance Framework and the third-party evaluator playbook show up, word for word, in EU or California regulatory text or guidance over the next two quarters. Proactive alignment converts to regulatory capture exactly through this mechanism: the regulated party writes the language the regulator ends up using.

- The S-1 timeline. If OpenAI files an S-1 in the next six to nine months and the governance section explicitly references this sprint of publications, the inference was correct. If the publications keep going monthly without an S-1, the IPO read was probably premature, but the regulatory-positioning read still holds.

The substance of the documents will be re-read for years. The timing is what tells you what they’re for.